New Construction Starts in November Slip 7 Percent

At a seasonally adjusted annual rate of $789.3 billion, new construction starts in November decreased 7% from October’s elevated amount, according to Dodge Data & Analytics. Most of the total construction decline in the latest month was the result of nonresidential building pulling back 15% after its 43% surge in October. There were eight very large projects with a value of $500 million or more (totaling $7.4 billion) that boosted nonresidential building in October. In contrast, there were just three very large projects with a value of $500 million or more (totaling $2.8 billion) that were entered as nonresidential building starts in November. The other two major construction sectors witnessed slightly reduced activity in November, with residential building down 1% and nonbuilding construction down 2%. During the January-November period of 2018, total construction starts on an unadjusted basis were $738.2 billion, up 1% from a year ago. Excluding the electric utility/gas plant category, which fell 30% year-to-date, total construction starts in the first 11 months of 2018 were up 2%.

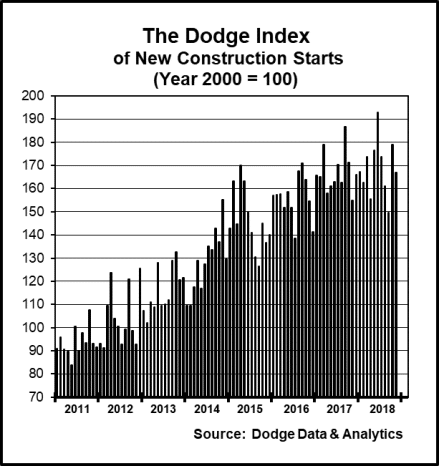

November’s data produced a reading of 167 for the Dodge Index (2000=100), down from a revised 179 for October and returning the Index to a level closer to the 166 average for the full year 2017. Through the first eleven months of 2018, the Dodge Index averaged 169. “Amidst the monthly ups-and-downs, the construction start statistics show that on balance the construction industry expansion was still underway in 2018, although the rate of growth has slowed considerably from the 7% gains for total construction reported during 2016 and 2017,” stated Robert A. Murray, chief economist for Dodge Data & Analytics.

November 2018 Construction Starts

“Several features stand out about the pattern of construction starts during 2018,” Murray continued. “Nonresidential building through eleven months has stayed within 2% of the enhanced activity registered during 2017, reflecting a varied performance by project type. The commercial building segment revealed more growth in dollar terms for hotels and office buildings, with the latter boosted by the start of such projects as the $1.8 billion Spiral office tower in New York, N.Y, a $665 million office tower on North Wacker Drive in Chicago, as well as several massive data center projects. The institutional building segment has benefitted from more growth for educational facilities and amusement-related projects, but transportation terminal starts have settled back from an exceptional amount in 2017 to what’s still a healthy volume in 2018. Manufacturing plant construction has shown wide swings month-to-month, yet for 2018 as a whole this project type continues to trend upward. With regard to residential building, multifamily housing has seen renewed growth in 2018 after its loss of momentum in 2017, but single family housing has essentially plateaued following the advances registered at the outset of 2018. For nonbuilding construction, the public works segment has shown growth for highways and bridges, helped by the 2018 federal omnibus appropriations bill passed back in March, although pipeline construction starts have eased back from a robust 2017. New electric utility/gas plant starts, despite the occasional jump such as reported in November, have continued to trend downward over the course of 2018.”

Comments are closed here.