The 2013 Utility Construction Outlook

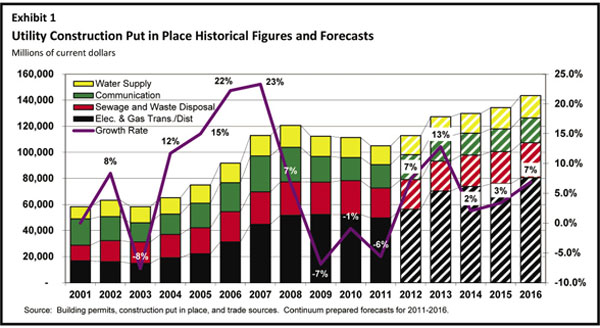

U.S. utility infrastructure is our greatest challenge and opportunity. The courage to make infrastructure investment by elected officials and agency leadership along with entrepreneurial ingenuity is required to navigate our volatile utility environment. The volatility is due to a combination of factors including: regulation; vast new finds of shale gas and oil; growth in natural gas as both a fuel for power generation and support for intermittent renewable power; clean water access and environmentally-sensitive wastewater treatment; and communications bandwidth to better connect individuals and organizations, as well as control infrastructure. In Exhibit 1 (next page), forecasted growth is positive, volatile and unbalanced. We anticipate a 13 percent peak in growth during 2013, followed by slow but accelerating growth through 2016. The growth over this time line is almost entirely related to one segment, electric and gas transmission or distribution.

Transmission and Distribution: Electric and Gas

The explosive growth of U.S. gas and oil production is fueled by hydraulic fracturing techniques causing unanticipated transformations. For the first time since World War II, less than 40 percent of U.S. power will be generated by coal with the bulk replaced by natural gas. The shift from coal is primarily driven by increasing regulation of coal plants and secondarily by the very low prices of natural gas since 2009. The exploration and production of natural gas and oil, as well as its use as a power generation fuel will, in the future, demand more pipeline construction.

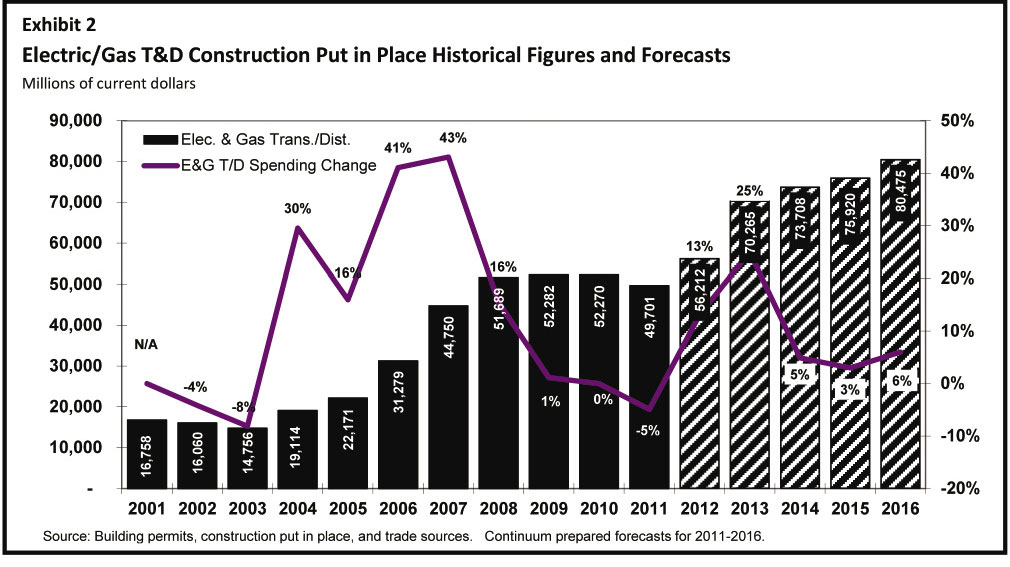

Today, spending growth in transmission and distribution (T&D) is driven by a combination of smart grid efforts, electric reliability, transmission pipeline integrity, distribution pipeline safety and replacement and exploration and production activity yielding rapid growth in 2012 and 2013 (Exhibit 2). Of particular importance is pipeline replacement to meet safety and integrity management requirements. Our experience shows that when utilities repair, upgrade or replace pipeline infrastructure, a three- to five-times increase in spending occurs.

Power generation is a future driver of T&D growth in the 2014-2016 time period. This late development is primarily due to the large amount of natural gas power plant capacity that was constructed in the late 1990s and early 2000s that is already supplied by existing pipelines. This large amount of unused capacity, and the flat electric demand in the United States driven by the weak economy, has allowed most utilities to avoid significant new pipeline construction to support gas-fired power generation. As the U.S. economy recovers, electric demand will rise and the supply and transmission issues will create more gas demand and ultimately pipeline construction activity.

Electric T&D construction slowed after the economic and financial crisis of 2008 and 2009 and the subsequently flattening of power demand. This infrastructure, however, holds great opportunity for upgrade through the application of communications technology and smart grid techniques and equipment. An acceleration of spending and growth in this sub-segment will occur once power demand increases and economic growth resumes.

Obstacles to increased spending still exist. The controversy over major electric transmission line permitting and construction, approval of the Keystone XL pipeline and rising backlash against fracking techniques offer examples of where courage is needed by elected officials, agency leadership and entrepreneurs.

Water Supply and Sewage and Waste Disposal

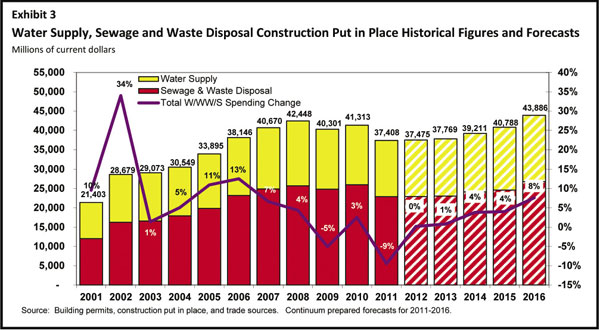

In the medium to long term, water will be one of the main challenges for the nation, and the municipal ownership for many of these systems presents unique opportunities for elected officials and agency leadership to demonstrate courage in the upgrade and investment in this infrastructure. In 2010, $36.4 billion in water infrastructure design, construction, materials, equipment and land rights spending took place in the United States. The Congressional Budget Office (CBO) estimates that $91.2 billion in spending was needed.1 This gap between need and spending, $54.8 billion in 2010, is projected to grow to $84 billion in 2020. Our forecast anticipates only 1 percent growth in 2013 construction as states, municipalities and the federal government grapple with tax, funding and debt issues (Exhibit 3).

U.S. water and wastewater systems are primarily municipally owned and highly fragmented with nearly 170,000 public drinking water systems and 16,000 wastewater systems. These systems rely on funding from local, state and federal sources in addition to their rate base. Meeting this funding shortfall will require a partnership of business and government to overcome past challenges, including the tendency of the federal government to place regulations and requirements on the state and municipal systems without providing the funding needed to meet these requirements.

Aging water and wastewater infrastructure is particularly a problem in the eastern United States and in older cities. A number of large- and mid-size cities continue to operate their wastewater systems under consent decrees. The 17 largest municipalities operating under consent decrees have a value in excess of $14 billion to be spent over a 10-plus-year time frame. As a result, spending in the wastewater market tends to exhibit a floor while water construction spending is more volatile.

From a demand perspective, water use in the United States has been relatively flat since 1985.2 Much of this is due to improvements in efficiency and conservation. The recent economic downturn, low housing growth and flat electrical power demand all have helped keep demand down. As the economy improves, water demand will increase. The connections between water and energy are broadening and deepening. For example, the rapid growth in hydraulic fracking, which uses up to 6 million gallons per day per well, is highlighting water and wastewater management.

The fragmented nature of the nation’s water and wastewater infrastructure and its funding requires leadership and courage by the elected officials, agency leadership and entrepreneurs that work in and for these systems. In the short-term, spending will continue to grow slowly as the economy and municipalities recover. This slow growth represents kicking the can down the road as the deficit of required spending grows by tens of billions. Only when business and government leaders have the courage to address the funding shortfall will significant spending growth occur.

Communications

Communications spending has historically been the most volatile of all utility segments. Today, the underlying fundamentals of this market revolve around unrelenting and increasing bandwidth demand that will help to mitigate the historic volatility of this market through the next down cycle in 2013-2015.

A trend is continuing where communication spending is becoming a larger part of overall Information Technology (IT) spending. One downside is that this shift will reinforce one type of volatility of communications infrastructure market as IT spending is closely linked to the overall business cycle. In contrast, another type of volatility can be decreased as communication spending becomes less tied to infrastructure spending which tends to move through overbuilding cycles.

The demand for increased bandwidth is driven by more than the needs of smartphones. The interconnected nature of modern IT devices creates a baseline of consistent demand growth for the communications industry that will serve as a ridged bottom that should mitigate the historic and extreme reductions in spending in this sector. Examples include:

1. Use of tablets, televisions, smart meters and smart infrastructure are just a few of the many devices that require an ever increasing amount of bandwidth.

2. Growth in cloud computing is expected to increase the portion of total IT spending tied to communication spending. From 2011 to 2017, the number of cloud computing subscriptions is forecast to grow from 300 million to 1.2 billion.3 This shift is reinforced by statistics describing telecommunications related IT spending. Globally, $3.6 trillion dollars will be spent on IT in 2012. The largest component of this spending is telecommunications related, accounting for 48 percent of the total ($1.69 trillion).4 Increase in bandwidth demand from 390 GB per month in 2011 to 440 GB per month in 2015 for heavy bandwidth users.5

3. Increase in demand from light bandwidth users will increase from 18 GB per month to 45 GB per month by 2015.6

One area not immediately driving high spending growth is the continuing build-out of fourth generation Long Term Evolution or 4G LTE networks.7 This construction type will not create a boom in overall spending, as much of the funds that were allocated to upgrade and expand the 3G networks were not spent in the 2010-2012 time period and are being moved over to support 4G. As a result, overall spending is relatively flat and should remain that way for some time.8

Another constraint to spending growth by rural and small telecom firms exists. In September 2012, the Federal Communications Commission (FCC) voted to “reconsider its long-standing limits on how many frequencies any one cell phone service provider can hold.”9 This comes at the same time that the FCC is encouraging television broadcasters to give up spectrum licenses for auction to wireless carriers. The availability of new spectrum combined with the possibility that large carriers, specifically AT&T and Verizon, could buy up large portions of the best frequencies, could severely limit the ability of small carriers to grow and slow this segment of communications-related spending.

Mark Bridgers and Nate Scott are consultants with Continuum Advisory Group, which provides management consulting, training and investment banking services to the worldwide utility and infrastructure construction industry. They can be reached at 919.345.0403 or MBridgers@ContinuumAG.com. For more information on Continuum, visit www.ContinuumAG.com.