A Contractor’s Guide to Construction in 2015

The Sun Is Out, Backlogs Are Growing and Contractors Feel more Optimistic

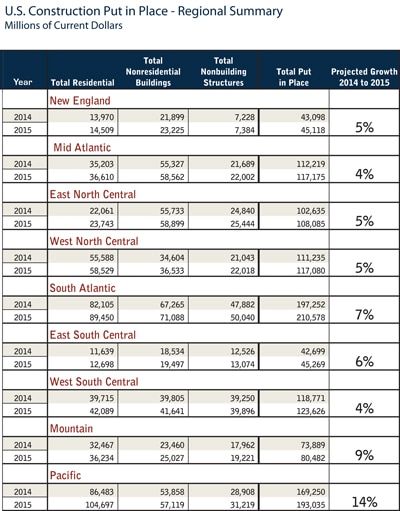

As Reagan said in his famous 1980 campaign speech, “It’s morning in America again.” The industry is recovering, and while many general contractors have not returned to peak levels, most are feeling more optimistic about future prospects than at any time during the last five years. FMI’s Nonresidential Construction Index (NRCI), which gauges contractor sentiment, currently reads 62.5 and has been in positive territory for 18 quarters in a row, dating back to Q2 2010. The most recent AIA Architecture Billings Index (ABI), which serves as a useful leading indicator for general contractors, tells us that new architectural design contracts have risen sharply in each of the past three months, and the pace of growth in June was the fastest in the roughly four years that the AIA has collected this data. This improvement seems to be reaching more balance across regions and across the major construction sectors. With the June ABI figures, firms in three of the four major regions of the country are reporting billings gains. [1]

Megaproject Proliferation and the Trend Toward Joint Ventures

Megaproject Proliferation and the Trend Toward Joint Ventures

Even with this positive news, the industry overall remains cautious about celebrating the recovery too soon. With prospects for contractors improving, a look inside the numbers indicates some trends worth noting. From 2005 to 2009, there were only 87 projects over $1 billion in size in the United States vs. the 2010 to 2014 period, which saw 336 projects over $1 billion. Conversely, nonresidential put-in-place spending from 2005 to 2009 totaled more than $3 trillion vs. $2.8 trillion for the 2010 to 2014 period. In other words, as the overall market was shrinking in size, the number of megaprojects was exploding. Since the vast majority of contractors lack the size or scale to compete for these megaprojects (which therefore go to megafirms and large joint ventures), the implication is that many firms were fighting for fewer and smaller projects.

As projects grow larger and owner demands become more complex across the general building market, partnering and joint venturing have become much more commonplace. Once the preserve of only the largest contractors and the largest projects, cross-firm collaboration has now become firmly entrenched in the lower and middle end of the construction market. Whether due to the social goals of public agencies (in meeting set-aside requirements), environmental and conservation requirements of private owners (LEED, etc.), the rapid expansion of subcontractor default insurance or a myriad of other factors, projects in today’s construction market require a greater level of cross-firm collaboration.

In this environment, the skill sets of successful contractors must be augmented with a new set of competencies. In particular, partner selection and project execution with partners must be a core skill of tomorrow’s successful general building contractor. Partnering and joint venturing are familiar concepts in the construction industry, but history is littered with failed efforts. Firms must develop a new set of evaluative tools to assist executives and project personnel to define the appropriate criteria and to measure successful outcomes. Successful firms learn from the mistakes of others and proactively employ strategies to ensure they can take advantage of the opportunities available through cross-firm collaboration.

Technology Advances (Too) Quickly Become Table Stakes

As noted in FMI’s “2014 U.S. Markets Construction Overview,” and as evident in any recent visit to a jobsite, the deployment of technology in the construction market is proliferating at a rapid rate. Advanced technology can be found in almost all elements of the construction process: project design, construction team coordination, field productivity enhancement, stakeholder information sharing and owner reporting. As mainstream adoption builds, expectations from project owners increase, and the use of technology becomes the norm rather than the exception. While general building firms undoubtedly are benefiting in many ways from these technological advances, they have not dramatically improved project margins or overall company financial performance. Rather, it is FMI’s observation that the financial benefits of technology adoption typically accrue to the owner rather than the contractor.

Why? The reasons are complex, but any analysis will conclude that at least one significant root cause is the persistence of the lowbid mentality of the construction industry. Efficiencies that are widely available to market participants soon become a requirement necessary to provide competitive levels of price and service. In other words, the use of advanced technology has rapidly shifted from being a unique differentiator for a few firms to a standard requirement for all.

A level playing field is created, and value migrates to those procuring services rather than the service providers themselves. In light of this, what can general building firms do to capitalize on technology? Certainly, the answer lies in increased utilization and a genuine recognition that business processes must change in order to complement available technology. In this way, market participants will distinguish themselves not by the use of technology, but rather through the proper application of process and technology to outpace competitors and deliver a higher-quality experience to customers.

As projects grow larger and owner demands become more complex across the general building market, partnering and joint venturing have become much more commonplace.

The Desperate Search for Differentiation

If “the many have been fighting for fewer and smaller” projects, and today’s competitive advantage is not sustainable forever, as outlined above, the need for differentiation has never been greater. Owners have used the recession and its ensuing years to gain advantage by becoming much choosier regarding contractor selection. As investment in the industry has increased, so have the pre-qualification standards for many owners. Long-standing local relationships are no longer sufficient, on their own, to win work. A phrase heard frequently from clients these days is “we had to go with the safe choice.” As a result, leading firms have beefed up business development efforts. Many contractors have discovered that a one-size-fits-all differentiation approach is difficult to attain: Every job and every owner is unique in their own eyes. A catchy slogan, tag line or me-too approach to differentiation rarely works. The firms that have fared best in recent years have figured out how to differentiate themselves on each job with that owner based on their objectives. This is not done easily and takes a proactive effort to gain positioning with the client early and set the table before an RFP hits the street.

The Strategic Significance of Risk Management

While the proliferation of contractor failures many predicted at the beginning of the recession has not proven out, the fact remains that construction is a high-risk proposition. Tight time frames, low margins, onerous contract terms, multiple stakeholders, subcontractor default risk and dangerous working conditions are all part of the program and are certainly not new. As a result, it is easy for general contractors to become numb to the risk. A compounding trend can be seen with insurable risk. In response to the recession, many insurance carriers had to increase prices and narrow coverages to offset lower returns on investment income. As the market continues to pick up steam, contractors are running hard and, ironically, increasing risk exposure while decreasing prices, leaving little margin for error.

As the landscape has changed, so has the role risk management plays inside many contracting firms. Rather than viewing risk as an unavoidable evil, firms have embraced risk management as a strategic opportunity. This adapted approach has contractors taking a holistic and strategic view of risk, while refining how to manage it to protect the balance sheet, improve operations, increase margins and mitigate the effects of an occurrence. Risk management is certainly not new to the construction industry, as employees across organizations manage multiple sets of risks on a daily basis. However, the focus among leading organizations has become much more intentional and formalized at an enterprise level.

Conclusion

The sun is out again and executive sentiment is at its highest level in many years. Backlogs are growing again, and contractors feel much more optimistic about future prospects. As the market has recovered, the industry has changed. Five years ago, BIM capabilities were a differentiator; now they are table stakes. Ten years ago, there were no billion-dollar projects; no one thought it possible the United States could ever be a net exporter of oil and gas, and there was no such thing as a data center market. Today, these are all reality. Leading firms have adapted to this changing landscape and must continue to do so in the future, as agility must become a core competence in the future. Contractors that invest resources and energy into being students of the industry, and the broader economy will continue to be successful.

Timothy R. Sznewajs is a senior managing director with FMI Capital Advisors Inc., FMI Corp.’s registered Investment Banking subsidiary. He can be reached at 303.398.7214 or via e-mail at tsznewajs@fminet.com. Scott B. Winstead is the president of FMI’s management consulting practice. He can be reached at 919.785.9249 or via e-mail at swinstead@fminet.com.