On the Road to Recovery

In the medium-duty truck business, the budding question on everyone’s mind is, “When will the market recover?” We’ll get to that, but first, it is important to understand where the market is now, how it got there and what it’s going to take to revive it.

ACT Research is uniquely positioned to answer the question as the aggregator of North American commercial vehicle statistics. Each month, all major OEMs report confidential market indicators, including new orders, cancellations, net orders, backlogs, inventories, production and retail sales, which ACT Research then converts into industry data. The forward-looking variables — backlogs, new and net orders and order cancellation rates — offer unique insights into short-term industry direction. Production and retail sales define current market and participant conditions.

ACT Research is uniquely positioned to answer the question as the aggregator of North American commercial vehicle statistics. Each month, all major OEMs report confidential market indicators, including new orders, cancellations, net orders, backlogs, inventories, production and retail sales, which ACT Research then converts into industry data. The forward-looking variables — backlogs, new and net orders and order cancellation rates — offer unique insights into short-term industry direction. Production and retail sales define current market and participant conditions.

Our research shows that a number of indicators impact demand for medium-duty trucks. Those metrics include but are not limited to consumer sentiment, manufacturing activity, employment and inflation. These factors then funnel into several other indicators that help define consumer behavior such as spending habits on goods, services and housing. Understanding the consumer is important for two reasons.

First, the vast majority of medium-duty truck buyers own small- and medium-size businesses and tend to exhibit a consumer mentality when purchasing vehicles. Second, those same buyers tend to own businesses that cater directly to consumers. And that’s a big deal, because consumer spending accounts for approximately 70 percent of total gross domestic product (GDP). Separate from that, spending on residential construction historically accounts for another 5 percent of GDP, though in 2009, that figure was a much lower 2.8 percent of GDP. Therein lies the crux of the issue that the medium-duty truck market has been contending with for the last three years.

North American medium-duty truck sales peaked in 2006, just shy of 190,000 units. In contrast, 2009 truck demand was less than half of the 2006 high, registering sales of just 74,000 units. The strong market in 2006 was framed by healthy GDP growth and easy access to capital. Part of the strength in GDP was being driven by a residential housing market that was just beginning to ease off its best performance ever. Consumers and businesses both took it for granted that the trend would continue. Hindsight now tells us differently. The housing bubble popped and it has been a downhill ride ever since.

North American medium-duty truck sales peaked in 2006, just shy of 190,000 units. In contrast, 2009 truck demand was less than half of the 2006 high, registering sales of just 74,000 units. The strong market in 2006 was framed by healthy GDP growth and easy access to capital. Part of the strength in GDP was being driven by a residential housing market that was just beginning to ease off its best performance ever. Consumers and businesses both took it for granted that the trend would continue. Hindsight now tells us differently. The housing bubble popped and it has been a downhill ride ever since.

As the general economy has slowed, so has the medium-duty market. Customers ordering and buying fewer trucks has resulted in numerous production cuts, layoffs and even the demise of two players in the space. The first to close its doors was Sterling Truck Corp., which had its genesis in 1997 when Freightliner Corp. purchased Ford’s heavy-duty truck business. Though Sterling was never a major player in the medium-duty segment during its brief 11-year life, it was a well respected brand among municipal and highway maintenance customers. Sterling’s last truck rolled off the line in March 2009.

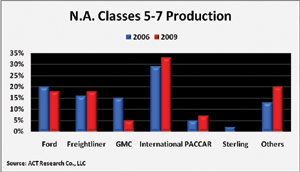

The second OEM to shutter operations was General Motors. After searching for more than four years for a suitable buyer, GM finally threw in the towel, ceasing production of its medium-duty product line on July 31, 2009. Sales are expected to continue through late 2010 as the company liquidates its existing inventory. GM’s exit will have long-reaching implications on the competitive landscape of the marketplace. Each of the remaining OEMs stands to gain some portion of GM’s customer base. The chart below shows the change in market share from 2006 to 2009, based on total North American production of all medium-duty chassis, including buses and RVs. As painful as it has been, the rationalization has been a necessary step along the path to recovery for the industry as a whole.

No doubt, you are familiar with the real estate axiom, “location, location, location.” The medium-duty truck industry has adopted a derivation of that mantra, calling for “construction, construction, construction,” to bring about the much needed recovery in the segment. The level of involvement of trucks in all phases of the construction process borders on phenomenal. Involvement starts with site preparation, requiring lots of earth-moving, trenching, asphalt, utility and concrete equipment, which is either mounted on or hauled by medium-duty trucks. Next comes the materials that are necessary for the project. Oftentimes, there are a few large deliveries that come by Class 8 trucks, but after those initial loads virtually everything else that is delivered to the site comes by medium-duty trucks. The list of contractors required to actually build a new home is endless. Most, if not all employ light- and/or medium-duty commercial vehicles to get the job done.

They include general contractors, builders, dry-wallers, plumbers, electricians, cable/telephone/Internet providers, finish carpenters, landscapers, etc. On a daily basis for several months, scores of workers using medium-duty equipment are onsite. Once the home is constructed, the owners move in and proceed to fill it with their worldly possessions, nearly all of which are delivered by, you guessed it, medium-duty trucks.

They include general contractors, builders, dry-wallers, plumbers, electricians, cable/telephone/Internet providers, finish carpenters, landscapers, etc. On a daily basis for several months, scores of workers using medium-duty equipment are onsite. Once the home is constructed, the owners move in and proceed to fill it with their worldly possessions, nearly all of which are delivered by, you guessed it, medium-duty trucks.

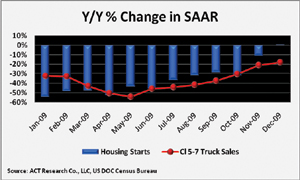

The correlation between various housing statistics and trucks sales is uncanny. The chart below shows that, at a seasonally adjusted annual rate (SAAR), housing starts began improving in January 2009. Five months later, Classes 5-7 truck sales also appear to have turned the corner. Note that, on a year-over-year basis, housing starts turned positive in December, while trucks sales were still negative. When we say they have started to improve, they are actually declining at a decreasing rate.

Given the amount of exposure medium vehicles have to housing and consumers, it is no surprise that the market has suffered. But all is not doom and gloom. Expectations are that the medium-duty truck market is set to begin its recovery in 2010. That expectation is based on an improving economy and a continuation of the housing market pick up that has been under way since early 2009. Taking these and other factors into account, ACT forecasts North American retail sales of 87,000 trucks in 2010. That represents an increase of about 20 percent over 2009 and is a good first step on the road to recovery.

ACT is the recognized leading publisher of commercial vehicle (CV) industry data, market analysis and forecasting services for the North American market. ACT’s CV services are used by all major North American truck and trailer manufacturers and their suppliers, as well as the banking and investment community. For more information on ACT, please visit www.actresearch.net.

Steve Tam is vice president of the Commercial Vehicle Sector with ACT Research, based in Columbus, Ind.

Comments are closed here.