Infrastructure Outlook

America’s economic competitiveness is under threat and the convergence of power, water and sewer infrastructure integrated through communication technology is one solution to an economic competitive advantage. This convergence matters because the ability to efficiently generate and distribute power combined with access to clean water integrated by highly effective communication technology can form the basis of the next generation of “American Exceptionalism.”

Unfortunately, the slowing economy has created fear that American competitiveness is evaporating. American competitiveness has always been based on the amount, quality and application of our resources leveraged by our infrastructure, not short-term economic vacillations. While our fundamental resources are robust, our infrastructure is rotting. President Obama alluded to this fact on September 8, 2011: “…We have to look beyond the immediate crisis and start building an economy that lasts into the future.”

More important than replacing aging utility infrastructure throughout America is recognizing that we stand at the verge of the next generation of “American Exceptionalism” — all we have to do is grab it. The convergence of critical infrastructure is an engine for American competitiveness, requiring the ability to efficiently generate and distribute power combined with access to clean water integrated by highly effective communication technology. Contractors that possess superior capabilities in two or more of these sectors are well positioned to thrive in 2012 and beyond.

Utility Construction Spending Forecast

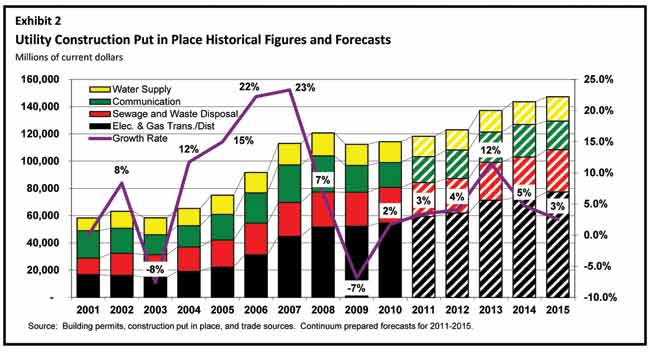

2012 will achieve modest growth overall with electric, gas and communication segments leading (Exhibit 1). Beyond 2012, growth is driven by a combination of improving economic fundamentals, regulatory required construction activity and pent up demand for the replacement or upgrade of capital assets. 2013 and 2014 represent a high watermark with only modest GDP growth anticipated through 2015. During the entire forecast period, water, wastewater and sewer sectors will grow but lag the overall growth rates due to funding challenges associated with the municipal ownership of these systems.

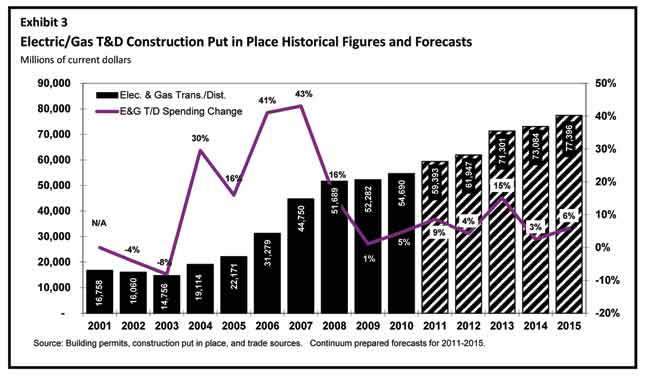

Transmission & Distribution – Electric and Gas

2012 will experience modest growth, driven by a combination of sources: 1) pipeline activity related to shale gas; 2) the conversion of coal fired power generation facilities to burn gas; 3) capital asset replacement; 4) regulatory compliance spending; 5) delayed infrastructure replacement; and 6) “Smart Grid” activity representing the convergence of power generation, transmission, distribution and communications technology requiring more skill than simply replacing a meter. All of these sources peak in 2013 and are unsustainable without an underlying GDP growth rate beyond 3 percent, which is not anticipated until the end of the forecast period (Exhibit 2).

One driver of transmission and distribution construction is a shift in power generation fuel mix. The transition away from coal towards natural gas and renewable sources is demanding transmission line construction, upgrade of substation infrastructure, pipeline construction and related activity. In a Black & Veatch1 forecast, the reduction in coal as a fuel is dramatic over a 20-year timeline and predominately replaced by natural gas. Assuming regulatory efforts to reduce or eliminate carbon emissions are successful, any type of stair step reduction will require robust use of natural gas. In addition, stable gas prices in the $4 to $6 range, are both very attractive to power generators and allow economic return from the shale basins.

The shift in fuel mix is driven by regulation and production or tax incentive. Coal fired plants are subject to no less than 10 different sets of regulations scheduled for implementation through 2017. These regulations involve: Ozone, SO2, NO2, Clean Air Interstate Act (CAIR), Water, PM2.5 (Particulate matter less than 2.5 micrometers in diameter), Ash, Hg (Mercury), Hazardous Air Pollutants (HAPs) and CO2.2 Other researchers argue that the planned and potential regulation is not burdensome and “…mostly consists of procedural events and activities that will not impose a direct compliance obligation on power plants.”3 This writer disagrees and finds that the net effect of these regulations is a tangled mess that restricts American competitiveness and will prevent power generators from making long-term, efficient bets with capital asset construction budgets reinforcing short-term, low risk decisions … albeit decisions that will generate transmission and pipeline activity.

Subsectors in This Market Include the Following:

Electric Transmission: Long-term prospects are very strong. Jon Wellinghoff, FERC Chairman, says: “Of the total miles of additional bulk power transmission, 50 percent is needed for reliability … 27 percent needed to integrate variable and renewable generation … The remainder is for integration of hydro, fossil-fuelled and nuclear generation and to reduce congestion … The existing transmission system was not built to accommodate this shifting generation fleet.”4

Electric Distribution: Variable growth dependent on a combination of new home construction in specific geographies, system age and replacement or renewal programs within a service territory and regulatory impact. One potential driver is the undergrounding of infrastructure to resist storms damage. A trend toward longer duration and larger outages increases the potential for undergrounding these assets.

Gas Distribution: Asset replacement recoverable under accelerated plans addressing pipeline integrity and safety concerns drive construction activity. Several of Continuum’s LDC clients have replacement budgets that increased five-fold since 2001. In addition, valve and system automation is driving activity.

Gas Submarkets and Gathering: “Fracking” and water demand represent hurdles likely to be resolved in favor of economic growth and job creation resulting in a robust and growing shale gas market. Low gas pricing is driving a shift of rigs from gas to oil production but it will not be as impactful as feared according to G. Allen Brooks, “…there has been a significant shift in the focus of drilling due to strong crude oil and weak natural gas prices … natural gas was only being targeted by 45.5 percent of working rigs … for crude oil, the industry has added 299 rigs…there are still significant volumes of natural gas produced from fields considered primarily oily or having high liquids content.”5

Gas Transmission: Given the low price of gas and economic conditions, transmission work has slowed and in some instances, pipelines are converting from gas to oil, illustrated by Kinder Morgan converting the Pony Express Pipeline. Long-term, the movement of shale gas to population centers and the conversion of coal fired power generation facilities to burn gas will energize this sector.

Liquids transportation: Natural gas liquids (NGL) emanating from the shale basins and oil constitute the majority of the growth in this sector. Oil prices at or above $80 per barrel demand more of this activity. As an example of NGL impact, “if U.S. output of ethane also rose 25 percent, it could spur $16 billion in new investment on U.S. chemical plants and create 17,000 jobs.”6

Water Supply & Sewage and Waste Disposal

The themes of convergence and competition pivot upon access to clean water and management of wastewater and sewage. Examples include the high volume water usage of “fracking,” the remote potential for “fracking” to contaminate water resources, additional requirements for hydro testing of pipelines and the high volume water usage in many power generation facilities. In contrast to controlling water usage, some districts and agencies view the water needs of these industries as an opportunity to sell water at a higher margin. Selling water at a higher margin is one solution to capital constrained municipal water, wastewater and sewage systems with empty municipal and state coffers, tight bond markets and low rates and use fees.

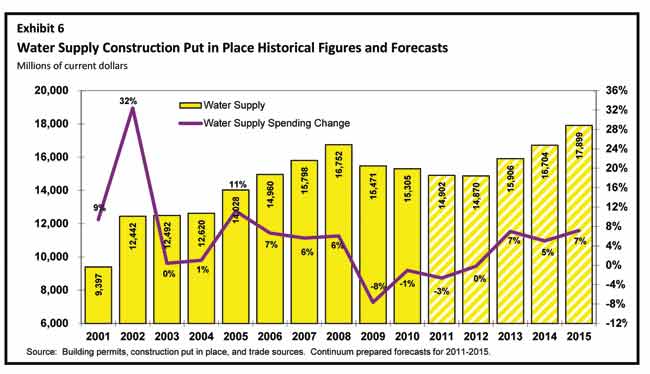

Water supply construction demonstrates a dramatic reduction of capital spending from 2008 with very limited prospects for improvement until 2013 due to these constraints (Exhibit 3).

The lack of recent spending on maintenance and upgrades will generate some capital spending growth regardless of economic conditions. A long running conflict between who writes and pays for regulations continues. Richard Anderson, representing the U.S. Conference of Mayors commented: “The Federal government [i.e., Congress and the relevant Federal Agencies] has performed one of the most sophisticated acts of avoiding responsibility for the policies it has imposed on the nation’s cities … the Federal government has abdicated its role as ‘partner’ in this effort … Congress has taken the position that achieving the goals of the water laws is not a federal responsibility.”7

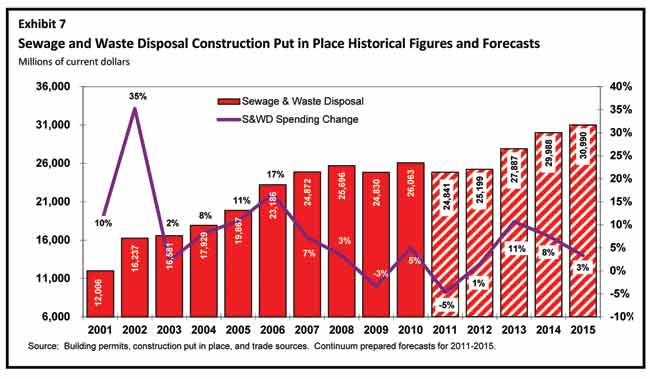

Aging infrastructure and environmental regulation are stronger spending drivers in the sewage and waste disposal sectors. In areas of limited supply, Denver, Los Angeles and Phoenix, push to increase the use of recycled water for irrigation, industry and agriculture. Goals call for a two to three times increase in recycled water use. Exhibit 4 demonstrates a less severe reduction in spending and faster recovery due in part to mandated work requirements.

There is no short-term fix for the operational and funding challenges facing water, wastewater and sewer systems that does not include higher rates and use fees. High unemployment, a weak housing market and the poor financial conditions of both state and local governments all contribute to the weakness of water and wastewater segments.

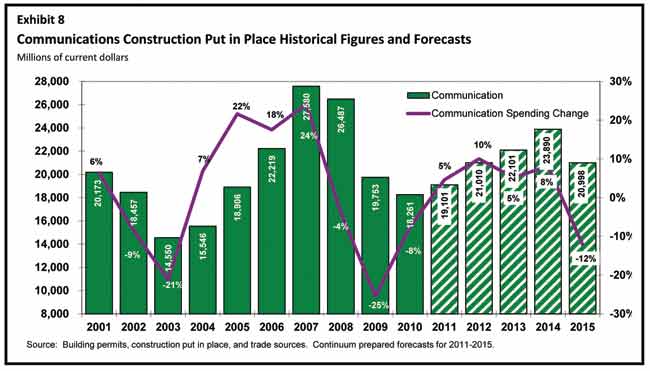

Communications

Communication is the most volatile utility industry segment. This creates an opportunity to either accurately anticipate how the market will evolve or be lucky enough to be in the right place. The current transformation of the industry is driven by three different developments: 1) growth in high bandwidth data streaming; 2) proliferation of smart devices allowing greater data usage; and 3) data centers to support cloud computing. Long-term, the convergence of power, water, sewer and communication infrastructure will generate new types of work for firms in this sector. As examples, accelerating installation of smart meters since 2007 and pending regulation requiring the installation of excess flow and remote control valves on gas or liquid pipelines will continue to create communication demands.

The forecasted increases from 2011 to 2014 are driven by the proliferation of devices requiring both high speed cellular networks along with Wi-Fi usage availability both at and away from home — all requiring greater data management and fiber-optic cable installations to meet customer reliability and speed demands (Exhibit 5).

The shape of the telecom market continually shifts. A Wall Street Journal article8 in 2011 presented the graphic detailing the tangled family tree of AT&T. The twists and turns depicted demonstrate the different business strategies that predominated over time ranging from monopoly, intense geographic competition, advent of wireless, consolidation and high volume data over broadband. The iterations demand industry participants to adapt their strategies, merge or die. This trend will continue and accelerate with the convergence of power, water, sewer and communication infrastructure. The forecasted drop in spending in 2015 anticipates that the market uncertainty is increasing and another transformation of the industry is taking place requiring industry participants to adapt, merge or die.

Conclusion

The necessary infrastructure for American competitive advantage changes over time and is shifting again favoring convergence of water, wastewater, power and communication infrastructure. In the previous 150 years, American entrepreneurs and farsighted government leaders transformed our country through canal and railroad transportation, a rapid industrialization, an unmatched highway system and a generation of technology innovation.

A new generation of American entrepreneurs and farsighted government leaders are required for the convergence of the power, water, wastewater and communication segments to take place. Of particular importance is access to clean water and wastewater management which serve as a pivot through which the next age of “American Exceptionalism” will originate but are where the greatest leadership challenges lay.

Utility engineers and contractors should take notice of the industry changes that are already underway and work to help their customers mitigate volatility they will face as the convergence described takes place. Said another way, utility engineers and contractors must become invaluable to owners by helping them attack the risks they face. Engineers and contractors that possess superior capabilities in two or more sectors are well positioned to thrive in 2012 and beyond.

There is room for significant optimism in 2012 and beyond founded on this writer’s belief that “American Exceptionalism” is alive and well.

Mark Bridgers and Nate Scott are consultants with Continuum Advisory Group, which provides management consulting, training and investment banking services to the worldwide utility and infrastructure construction industry. They can be reached at (919) 345-0403 or MBridgers@ContinuumAG.com for more information on Continuum, visit www.ContinuumAG.com.

- Black & Veatch, What Will Be the North American Energy Industry’s “New Normal,” November 17, 2010, pg. 21.

- Edison Electric Institute, adapted from Wegman EPA 2003 report and updated on February 15, 2010. Downloaded from www.EEI.org on October 10, 2011.

- World Resources Institute, WRI Fact Sheet, Response to EEI’s Timeline of Environmental Regulations, November 2010, pg. 2.

- Wellinghoff, John, Statement of Chairman Jon Wellinghoff on Transmission Planning and Cost Allocation, Docket No. RM10-23-000, July 21, 2011.

- Brooks, G. Allen, Parks Paton Hoepfl & Brown, North American Outlook & Insights News: Whither The Direction of Natural Gas Markets, September 14, 2011.

- Clanton, Brett, Houston Chronicle, Natural Gas Boom Helps Petrochemical Industry, March 23, 2011. Downloaded from www.chron.com on October 10, 2011.

- Anderson, Richard F., The U.S. Conference Of Mayors, Trends in Local Government Expenditures on Public Water and Wastewater Services and Infrastructure: Past, Present and Future, February 2010, pg. iii

- Raice, Shayndi, Wall Street Journal, AT&T Outguns Sprint, March 29, 2011. Downloaded from http://blogs.wsj.com/deals/2011/08/31/atts-tangled-family-tree/ on October 10, 2011.