Infrastructure Outlook

American infrastructure, particularly utility infrastructure, faces a host of factors that impact design and construction activity. One of the most important is governmental oversight, regulation and funding influences. As pressure mounts to resolve the economic and financial turmoil, many eyes look to Washington and state capitals for solutions. In FMI’s 2010 overview of the utility construction market, the focus is on understanding the impact and influence governmental agencies are having on utility construction.

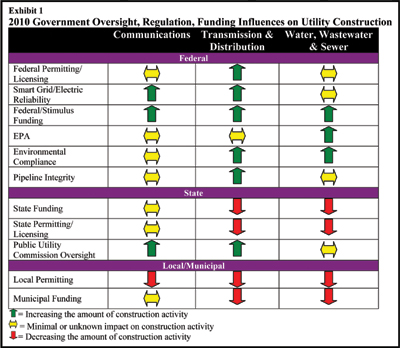

Exhibit 1 describes eleven different ways that utility construction is influenced from the federal, state and municipal levels. This list is not all inclusive, yet it represents the areas FMI believes are of greatest impact. FMI is not passing judgment on whether the impact is positive or negative; rather, the arrow indicates whether or not we believe it is creating or restricting additional construction activity.

Exhibit 1 describes eleven different ways that utility construction is influenced from the federal, state and municipal levels. This list is not all inclusive, yet it represents the areas FMI believes are of greatest impact. FMI is not passing judgment on whether the impact is positive or negative; rather, the arrow indicates whether or not we believe it is creating or restricting additional construction activity.

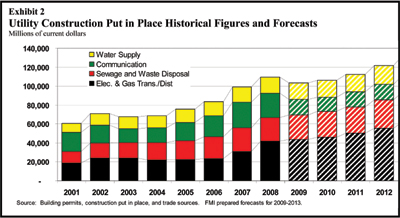

Overall, FMI expects governmental influences to help generate some growth in construction activity in 2010 (Exhibit 2). With the exception of communication, FMI forecasts all utility market segments to finish 2009 and 2010 with equal or more construction put-in-place than in 2008. This growth is not necessarily balanced within a market sector and will appear different for every contractor. As an example, the growth in transmission and distribution construction is very unbalanced. Both gas and electric new service construction is essentially non-existent, while electric transmission and pipeline replacement work is exhibiting significant growth.

On March 25, 2009, the American Society of Civil Engineers (ASCE) published their bi-annual assessment of U.S. infrastructure. No surprise, the “Five Key Solutions” put forward to address aging infrastructure are further intensifying the focus on Washington and state capitals. The number one solution calls for, an “Increase Federal Leadership in Infrastructure.” 1

Transmission & Distribution

Transmission and distribution construction has been the focus of much attention as a result of President Obama’s promise to upgrade our ailing grid and create a “green” superhighway for power. But is a high-voltage transmission system built to accommodate renewable energy wishful thinking? FMI forecasts 6 percent growth in T&D-related construction in 2010, but not the eye-popping figures hoped for by the engineering and construction community. The overall growth rate for this segment won’t begin aggressive acceleration until the housing inventory is absorbed, which FMI does not anticipate until 2011.

Electric T&D

With the grid approaching capacity and more power set to come online, the Department of Energy’s (DOE) Office of Electricity Delivery and Energy Reliability has partnered with the industry to begin shoring up transmission lines using high-temperature superconducting (HTS) cables. The first such project was completed in April 2008 when the American Superconductor Corp. (AMSC) and Long Island Power Authority (LIPA) energized a 2,000-ft, 138-kV cable capable of transmitting 574 megawatts of energy. The project’s cost of $58.5 million was subsidized to the tune of $28.5 million by the DOE. More testing of this technology to address upgrade and replacement will take place. As an example, currently underway is a $39 million project on New York City’s network, operated by ConEdison. Dubbed “HYDRA,” the project is dependent on the Department of Homeland Security (DHS) for $25 million in funding.2

With the grid approaching capacity and more power set to come online, the Department of Energy’s (DOE) Office of Electricity Delivery and Energy Reliability has partnered with the industry to begin shoring up transmission lines using high-temperature superconducting (HTS) cables. The first such project was completed in April 2008 when the American Superconductor Corp. (AMSC) and Long Island Power Authority (LIPA) energized a 2,000-ft, 138-kV cable capable of transmitting 574 megawatts of energy. The project’s cost of $58.5 million was subsidized to the tune of $28.5 million by the DOE. More testing of this technology to address upgrade and replacement will take place. As an example, currently underway is a $39 million project on New York City’s network, operated by ConEdison. Dubbed “HYDRA,” the project is dependent on the Department of Homeland Security (DHS) for $25 million in funding.2

As NRG Energy CEO David Crane explains, “If we are not doing things completely differently by 2030, we will be in a world of hurt.”3

The American Recovery and Reinvestment Act (ARRA), better known as the stimulus program, appropriated $6 billion to support the DOE’s loan guarantees of $60 billion for renewable energy and electric transmission projects. While undoubtedly a noteworthy and positive measure, utilities and transmission developers are having trouble obtaining permit approval to site and build transmission lines. Standing in their way is a maze of both state and federal regulations, with the two sets often misaligned.

In California, a state known for their progressive stance on regulating transmission construction, Governor Schwarzenegger announced that he would veto legislation requiring 33 percent of the state’s energy to come from renewable sources by 2020, instead choosing to mandate the change through executive order. His action is out of concern for what his communication director called a “poorly drafted, overly complex bill…that will kill the solar industry in California and drive prices up like the failed energy deregulation of the late 1990’s.”4 The source of the conflict was a provision that allowed California utilities to buy power from outside the state.

Liquids and Natural Gas

The rock-bottom natural gas prices and expanding domestic supply will lead to mixed construction activity for liquids and natural gas markets. Though extraction activity has slowed as natural gas price has fallen, pipelines are still being constructed to support additional generation capacity from a cheap, relatively clean fuel source. The various forms of natural gas have very few or only one carbon atom, making it the cleanest fossil fuel in terms of carbon emissions (See Exhibit 4).

The rock-bottom natural gas prices and expanding domestic supply will lead to mixed construction activity for liquids and natural gas markets. Though extraction activity has slowed as natural gas price has fallen, pipelines are still being constructed to support additional generation capacity from a cheap, relatively clean fuel source. The various forms of natural gas have very few or only one carbon atom, making it the cleanest fossil fuel in terms of carbon emissions (See Exhibit 4).

A June report from the Potential Gas Committee out of Golden, Colo. estimated U.S. reserves of natural gas to be 35 percent higher than two years ago — thanks to new technology that allows extraction from shale.5 The Rockies Express Pipeline has been expanding eastward to bring the fuel from the Rocky Mountain gas fields to more developed markets in the east. Shale gas usage has grown and now accounts for approximately 5 percent of total U.S. production, according to the Gas Technology Institute (GTI).

Over the long-term, FMI expects growth in the pipeline construction market to support bringing this gas on line even while more stringent environmental and permitting requirements may slow or lengthen this effort. According to Neil Ellerbrook, Chairman and CEO of Vectren Corp., “Our industry will probably see more regulation, especially in the area of access to new natural gas supply. On the other hand, given the fact that our customers have been leaders in energy efficiency and conservation for the past 40 years, we are well positioned…”6

The growth in domestic gas production in the United States over the last three years has raised the visibility of both GTI and the American Gas Association (AGA). In the case of the AGA, they have selected five major themes in their strategic plan, the first of which encourages a “new, modern world in the regulatory environment.” As AGA Chairman Skains explains, the regulatory framework in place promotes increasing energy use in a time when energy use is decreasing. He goes on: “We need to work with our regulators on regulatory innovation that doesn’t punish utilities for promoting conservation and efficiency, but rather rewards them.”7

The growth in domestic gas production in the United States over the last three years has raised the visibility of both GTI and the American Gas Association (AGA). In the case of the AGA, they have selected five major themes in their strategic plan, the first of which encourages a “new, modern world in the regulatory environment.” As AGA Chairman Skains explains, the regulatory framework in place promotes increasing energy use in a time when energy use is decreasing. He goes on: “We need to work with our regulators on regulatory innovation that doesn’t punish utilities for promoting conservation and efficiency, but rather rewards them.”7

Water Supply

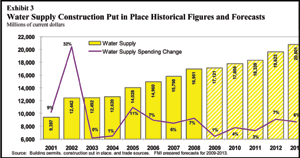

Water supply construction growth is flat for 2009 and FMI is forecasting a 4 percent growth rate in 2010, in part buoyed by stimulus funding. According to the aforementioned ASCE 2009 Report Card, the United States needs to spend an additional $11 billion per year to maintain our current water infrastructure at only it’s current functioning level and requires as much as $1 trillion over the next 20 years to improve functioning.

Water supply construction growth is flat for 2009 and FMI is forecasting a 4 percent growth rate in 2010, in part buoyed by stimulus funding. According to the aforementioned ASCE 2009 Report Card, the United States needs to spend an additional $11 billion per year to maintain our current water infrastructure at only it’s current functioning level and requires as much as $1 trillion over the next 20 years to improve functioning.

A 2007 Environmental Protection Agency (EPA) study indicated a need of $334 billion for water supply infrastructure over the next 20 years. This marks a $134 billion increase over the forecast when the study done ten years earlier. 8 Water supply trade associations consider the EPA conservative and have issued forecasts that demand much higher levels of investment. Regardless of which study you subscribe to, the demand far exceeds the currently available funding sources. Rather than expound on the massive spending deficits in water supply infrastructure, FMI outlines some examples of construction activity that is occurring and the opportunities available to optimistic contractors.

Movement toward low-impact or “green” infrastructure solutions such as rain barrels, green roofs, porous pavement and other strategies to retain rainwater onsite are also creating a retrofit market for water supply contractors.

As with other utility segments, federal investment is crucial. The Journal of American Water Works Association (AWWA) has described the U.S. water regulations as an “immense maze and administrative superstructure that…may be at risk of collapsing under its own weight.” But according to the 2009 Water Industry Report, “It is these regulations which really drive the day-to-day activities, spending levels and commercial developments in the water industry. Since 9/11, growing concern for contaminants creates new opportunities for water testing companies.”

Without federal financial support, FMI does not see a scenario in which the needed spending and improvements can occur. The real question that remains is exactly how the necessary federal investment will be distributed and filtered down to the municipalities that manage water supply infrastructure. Unfortunately, many share the pessimistic view that only with a catastrophe will we see real change of policy.

Sewage and Waste Disposal

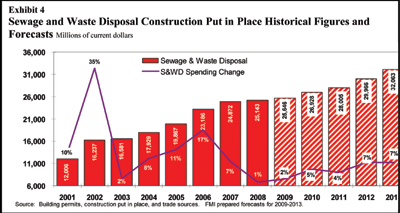

The Sewage and Waste Disposal market is also exhibited very modest growth in 2009, with a 2 percent increase forecast. This will likely be followed by more substantial expansion in 2010 at 5 percent. As more and more municipal sewer systems reach the end of their useful life, the primary source for funding their repair and upgrade (State Revolving Loan Fund) has remained flat for over a decade. Though substantial funding gaps are beginning to snowball, all hope should not be lost. The 2002 EPA Gap Analysis estimated that just a 3 percent increase over currently forecast wastewater construction spending would reduce the roughly $6 billion annual gap by 90 percent.9

The Sewage and Waste Disposal market is also exhibited very modest growth in 2009, with a 2 percent increase forecast. This will likely be followed by more substantial expansion in 2010 at 5 percent. As more and more municipal sewer systems reach the end of their useful life, the primary source for funding their repair and upgrade (State Revolving Loan Fund) has remained flat for over a decade. Though substantial funding gaps are beginning to snowball, all hope should not be lost. The 2002 EPA Gap Analysis estimated that just a 3 percent increase over currently forecast wastewater construction spending would reduce the roughly $6 billion annual gap by 90 percent.9

In 2009, the EPA announced that it plans to increase the standards for water discharged by coal-fired power plants. An EPA study completed this year concluded that current power plant wastewater discharge regulations have not kept pace with the electric power industry. Specifically, air pollution controls meant to curb CO2 emissions require the “scrubbing” of boiler exhaust with water, and when the process is not properly managed, contaminated water is released to rivers and other bodies of water. The EPA study that reports these findings will be released later this year, at which time more stringent wastewater discharge standards will be implemented.10

In the American southwest, engineers have managed to keep the valuable Colorado River free of salty farm runoff by diverting it south of the border to Mexico. An accidental result is a vibrant wetland called the Cienega de Santa Clara. Now the western states see this runoff as a potential solution to the drought. A $256 million desalination plant in Yuma, Ariz. has been virtually inoperable since it was built 17 years ago. This plant would allow Western states to preserve water for use.11

Communications

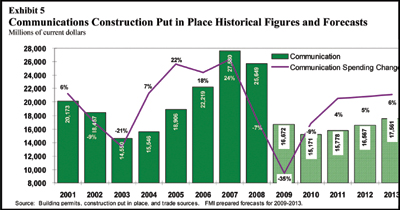

FMI forecasts 2009 will close with communication construction spending down 35 percent, as compared to 2008. This drop of nearly $9 billion in put-in-place work is not unexpected and is projected to continue into 2010 with an additional drop of 9 percent. As we discussed in last year’s utility construction outlook, these relatively wild swings in communications-related spending are not unexpected as the communications market tends to amplify broad economic swings because of the quick-turn and fast-pace of many communications infrastructure projects.

FMI forecasts 2009 will close with communication construction spending down 35 percent, as compared to 2008. This drop of nearly $9 billion in put-in-place work is not unexpected and is projected to continue into 2010 with an additional drop of 9 percent. As we discussed in last year’s utility construction outlook, these relatively wild swings in communications-related spending are not unexpected as the communications market tends to amplify broad economic swings because of the quick-turn and fast-pace of many communications infrastructure projects.

Mobile infrastructure will likely lead the way as communication-related construction looks to rebound. According to a new report by ABI Research,12 even under the worst recovery scenarios mobile service revenues should continue to grow at roughly 1.2 percent annually through 2014.13 Even communications construction growth will not occur without governmental impact. As stimulus packages bolster Asian-Pacific communications firms, it may increase their ability to compete in North America.

Despite the tempered growth in many utility construction markets over the next year, the industry still faces the same problems as the general economy.

But unlike America’s private companies, utilities have long been guided by governmental and regulatory pressures. Perhaps this is why Americans who revile at the thought of state-controlled enterprise in industries such as banking and insurance are happy to put pressure on Washington to improve our nation’s utility infrastructure. In closing, President John F. Kennedy reminds us of the unique environment that utilities will be forced to navigate:

“Washington is a city of Southern efficiency and Northern charm.”

Mark Bridgers and Dan Tracey are Consultants with FMI Corp., which provides management consulting, training and investment banking services to the worldwide construction industry. They can be reached at (919) 785-9351 or MBridgers@fminet.com for more information on FMI, visit www.fminet.com.

Comments are closed here.