Finding the Silver Lining

With a struggling economy making fast, easy credit something of the past and banks refusing to lend to one another, the hopes of a contractor securing credit can be questionable. Utility systems and owners, however, are another story. Through large, multi-year projects where financing is typically secured in advance, these owners and systems are partially protected from the credit crisis — at least in the short term. FMI continues to forecast growth in the transmission and distribution, sewer/wastewater, water supply and communications infrastructure and utility segments for 2009. This growth is in part due to these large, multi-year projects where financing is secured, as well as demand increases to address aging infrastructure and needed system enhancement.

With a struggling economy making fast, easy credit something of the past and banks refusing to lend to one another, the hopes of a contractor securing credit can be questionable. Utility systems and owners, however, are another story. Through large, multi-year projects where financing is typically secured in advance, these owners and systems are partially protected from the credit crisis — at least in the short term. FMI continues to forecast growth in the transmission and distribution, sewer/wastewater, water supply and communications infrastructure and utility segments for 2009. This growth is in part due to these large, multi-year projects where financing is secured, as well as demand increases to address aging infrastructure and needed system enhancement.

FMI is in the process of updating its forecasting model to reflect the implications of the stock market meltdown in early October 2008. The forecasts do not yet take into account these shifts, and FMI anticipates a softening of growth rates in these infrastructure and utility markets throughout 2009 and 2010 where significant long-term, reasonably priced credit for utility systems and owners will be more difficult to secure. The high volatility in the stock and credit markets will result in greater volatility in construction spending. FMI does however see a silver lining due to the increasing need to address aging infrastructure, as well as a congressional shift toward potentially greater funding of infrastructure construction, which serves as an investment for governmental agencies rather than consumption.

Transmission and Distribution

The construction put in place for the underground transmission and distribution market increased (9 percent) to almost ($29.6 billion) in 2008, and FMI forecasts an additional increase of (5 percent) in 2009. Power-related transmission and distribution, in comparison to other utility infrastructure segments, is the most resistant to downward pressure from the financial markets due to the size, cash flow and relative good credit standing of many firms. They are not insulated from continuing political gridlock surrounding legislation or regulation to encourage investment in the nation’s rapidly aging infrastructure. FMI believes that the new political administration, whichever party is elected, will again work to attempt to address the structural, industry and regulatory flaws that make it harder and less financially rewarding to replace this infrastructure.

Investment in transmission projects will continue at an aggressive pace, in part because of financial support from federal and state regulated rates of return. Electric transmission-related spending will be partly driven in the western states by renewable energy generation as new transmission lines must be built for interconnection to the grid. The Federal Energy Regulatory Commission (FERC) has offered higher rates of return for some larger projects as well, to spur transmission construction.

According to the Edison Electric Institute, U.S. transmission capacity has not kept up with rising electricity demand, which has increased 20 percent over the last decade. Despite the social and political pressure for utilities to upgrade their transmission infrastructure, there is relatively little financial incentive offered by such upgrades. Nonetheless, many large utilities such as NiSource, Exelon and AEP have announced large capital campaigns during 2008 to combat aging transmission and distribution infrastructure.

Domestic natural gas production grew by over 4 percent in 2007 and is already up 9 percent in the first quarter of 2008 due in part to new technology that allows firms to tap previously inaccessible gas trapped in existing coal and shale mines. In the United States, demand for natural gas continues and its availability in North America makes it attractive for drilling, exploration and ultimately transmission-related projects to support getting the gas to market.

Domestic natural gas production grew by over 4 percent in 2007 and is already up 9 percent in the first quarter of 2008 due in part to new technology that allows firms to tap previously inaccessible gas trapped in existing coal and shale mines. In the United States, demand for natural gas continues and its availability in North America makes it attractive for drilling, exploration and ultimately transmission-related projects to support getting the gas to market.

Escalating and highly variable materials costs will continue to alter utility construction in 2009, just as they did in 2008. According to the Handy-Whitman Index of Public Utility Construction Costs, T&D costs have increased an average of 4.8 percent and 5.4 percent per year, respectively, since 2003. Just as copper prices peaked during 2007 and showed some signs of steadying in 2008, steel became highly variable. From June to July of 2008, for example, steel prices saw a 30 percent rise.

Sewage and Waste Disposal

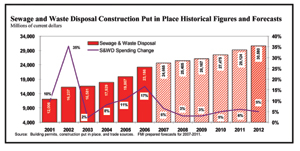

Projected 2009 spending on wastewater construction will total $26.2 billion, an increase of 3 percent from 2008 (see graph above). Even with forecasts showing in excess of $25 billion in wastewater spending until 2012, industry groups still predict funding gaps to grow to between $200 billion and $1 trillion over the next two decades. The credit crisis will tend to hit these municipal utility systems more aggressively due to their frequent reliance on short-term credit facilities to fund capital construction. The absence, tightening or increased cost of these facilities will further stifle spending growth in a segment that historically has difficulty securing adequate funding.

The 16,000 U.S.-based sewage and water treatment systems will continue to struggle with deteriorating infrastructure in 2009. Rehabilitation of the aging pipe systems will remain among the top wastewater needs for the near future. Additionally, wastewater treatment plants face continuous facility improvement needs to meet increased water quality standards. Issues surrounding combined sewer overflows (CSO) and sanitary sewer overflows (SSO) have given rise to an insurmountable funding gap for the entire nation.

According to the Environmental Protection Agency (EPA), almost equal shares of the estimated immediate capital needs for wastewater construction are for wastewater treatment systems ($69 billion; 34 percent) and wastewater collection and conveyance ($65 billion; 32 percent). CSO and SSO corrections account for 27 percent ($54 billion) of the capital needs. Not surprisingly, states with larger populations and/or the oldest operating systems are facing the greatest need for wastewater construction. New York, California, Illinois, Ohio and Florida are the top five states with the largest funding needs for wastewater construction and treatment.

Majority needs for these top five states:

- New York — Advanced wastewater treatment

- California — Secondary wastewater treatment

- Illinois — Sewer replacement/rehabilitation and CSO correction

- Ohio — Infiltration/inflow and CSO correction

- Florida — Advanced wastewater treatment

Together, these five states make up almost 40 percent of the reported $200 billion needed to improve the nation’s wastewater infrastructure. Federal funding for wastewater construction will remain limited and local communities and municipalities will inevitably bear this burden. Local taxpayers, already stretched by increased spending needs related to other aging infrastructures (water and transportation), will have to make funding allocation decisions with limited resources.

Water Supply

Capital spending in the water supply utility segment is largely a function of macro-economic trends. For example, the drastic slowdown on new home starts will prevent significant growth in the water supply and municipal pipe work sectors. FMI forecasts an estimated growth rate of 2 percent in 2009 for water-related markets. Total construction spending will be roughly $15.7 billion in 2009. Water supply construction is expected to have slow, steady growth from 2010 to 2012 that outpaces inflation. FMI is currently forecasting increasing growth in housing construction for 2010, which is the underlying driver for growth in water supply construction.

Funding shortfalls and inaction by governing bodies on all levels will continue to exacerbate the current conditions in water construction. Regulators and government entities have acknowledged the problems; however, the majority of current spending is representative only of stopgap fixes. The EPA estimates that the United States will continue to see a funding gap of more than $100 billion over the next 20 years. As with the other utility segments, funding gaps will continue to grow until alternative and innovative financing models are explored and accepted by public and private stakeholders.

Communications

There are few industries as highly linked to innovation as communication. It is logical, therefore, the communications-related capital spending is driven by the pace and implementation of technological advancement. In 2009, FMI forecasts a modest 2 percent growth as telecommunications companies look to capitalize on large capital improvement plans from the past couple years. The conservative lending that will no doubt characterize 2009 will significantly limit growth in the highly speculative telecom sector. Fiber-optic cable installation led a wave of construction in the late 1990s, wireless infrastructure dominated spending throughout the early 2000s and recently upgraded fiber-optic cable has driven communication spending.

Recent upgrades to existing fiber systems have allowed communication service providers to offer expanded internet bandwidth, basic and high definition television programming and VoIP telephone services in an all-in-one package. Today’s fiber-optic cable networks are called fiber-to-the-node (FTTN) networks and run fiber optics to a neighborhood or a business park’s network of low-tech copper cable. Trends in fiber service bundles and various reports on cost savings through fiber data-transfer technology and Voice over Internet Protocol (VoIP) telephony indicates that the industry will continue to lean heavily on fiber optics over the next five years. FMI expects this trend to place downward pressure on future investment in traditional landline-phone infrastructure construction, forcing established telephone companies to weigh the long-term sustainability and profitability of the service.

Recent upgrades to existing fiber systems have allowed communication service providers to offer expanded internet bandwidth, basic and high definition television programming and VoIP telephone services in an all-in-one package. Today’s fiber-optic cable networks are called fiber-to-the-node (FTTN) networks and run fiber optics to a neighborhood or a business park’s network of low-tech copper cable. Trends in fiber service bundles and various reports on cost savings through fiber data-transfer technology and Voice over Internet Protocol (VoIP) telephony indicates that the industry will continue to lean heavily on fiber optics over the next five years. FMI expects this trend to place downward pressure on future investment in traditional landline-phone infrastructure construction, forcing established telephone companies to weigh the long-term sustainability and profitability of the service.

In order to mitigate the loss of landline customers, Verizon, for example, has been heavily investing in its own proprietary fiber-optic service (FiOS) network. The $26 billion fiber-optic infrastructure is expected to be complete in 2010 and will allow Verizon to replace a neighborhood’s or business park’s low-tech copper communication infrastructure with high-speed fiber optics. Generally speaking, the rapid technological advancements in fiber optics have slowed in recent years as the communications industry has trends such as off-shoring and consolidation.

Conclusion

An economic slowdown and restricted credit will characterize the first half of 2009. The underground utility construction market offers a silver lining as one of the only markets anticipating growth in construction spending in 2009. While 2009 will no doubt bring with it many unpredictable events, utility contractors can rest assured that construction will move forward in their industry, albeit with greater competition, and work will be available for those firms that can win it.

Mark Bridgers, Mike Chase and Dan Tracey are consultants with FMI Corp., which provides management consulting, training and investment banking services to the worldwide construction industry. They can be reached at (919) 785-9351 or MBridgers@fminet.com. For more information on FMI, visit www.fminet.com.

Comments are closed here.