Equipment Indemnity

Any piece of equipment is a substantial investment. Whether it’s a compact $30,000 skid steer or a massive $100,000 excavator, it’s a necessary tool that helps you get your job done. And that’s an investment that you want to protect. Equipment insurance coverage is designed to cover the mobile construction equipment you use every day on your jobsite, and it applies to the direct physical loss of the equipment.

“Coverage applies to equipment owned by the insured but can be extended to equipment rented or borrowed from others,” says Jayne Honeck, AVP Underwriting for the Inland Marine division of CNA Insurance.

There are a myriad of insurance options, so you want to make sure that you have the right coverage for your machines and their applications. To start with the basics, equipment coverage can be written as a monoline policy (insurance protection written in the form of a single policy) or lumped together as part of a package, with or without liability coverage.

There are a myriad of insurance options, so you want to make sure that you have the right coverage for your machines and their applications. To start with the basics, equipment coverage can be written as a monoline policy (insurance protection written in the form of a single policy) or lumped together as part of a package, with or without liability coverage.

“The [contractor equipment] portion of either a monoline or package policy typically provides coverage on equipment for the majority of risk perils,” says Bruce Bitler, Field Vice President for Zurich North American Commercial Construction. “Some policies have restrictions regarding the perils of flood, windstorm or machinery breakdown. For example, coverage can be expanded by endorsement to provide rental reimbursement, including extra expense and continuing rental expense if the equipment is damaged or destroyed, allowing the insured to get back to work as soon as possible.”

As a utility contractor getting into the nitty-gritty of specific insurance offerings, you want to take a look at your usual applications and tailor a policy that fits the risks involved.

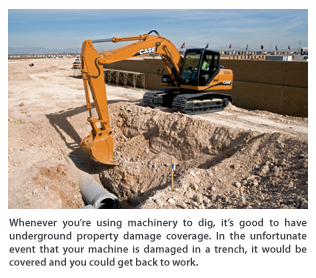

“Anytime you deal with underground utilities, you want to make sure that you have coverage for property underground,” says Joseph Tracy, President of Travelers Inland Marine. “That would go hand in hand with utility contractors. A lot of times the contractor might have some specific equipment designed for the job and if there were a loss of that equipment, you’d want to make sure that they have rental insurance that they can go out and find a substitute piece of equipment to continue their job.”

If you’re digging or drilling, you want the insurance policy to include underground property damage because it’s an inherent risk with that type of operation. In layman’s terms, if your equipment is damaged while underground — be it a drill or an excavator that falls into a trench due to a collapse — you want any damage that your machine takes to be covered.

Another major coverage policy to take a look at is rental and leasing coverage options. There are times when you have a buddy on a job and he needs to borrow a backhoe loader. These deals are often casual verbal agreements between two professionals, which are all well and good until the equipment is damaged. It’s a good idea to check your policy to see what equipment is covered. The borrower might think his insurance will cover the machine if it’s damaged, but in actuality, he could only be covering the equipment that he owns. When you’re in that situation, it’s a good idea to provide a written rental agreement beforehand that spells out who is responsible for what.

Rental reimbursement coverage is also a good policy to have. It pays the rental amounts to temporarily replace a piece of covered equipment that has suffered damage from a covered cause of loss, up to a specified limit, according to Honeck.

It’s also possible to add business income, contractual penalties and extra expense coverage. That’s for when a piece of covered equipment is lost or damaged due to a covered cause of loss and the result is that a job cannot be completed. Of course that means a loss of income or a contractual penalty. This coverage will pay the net income that would have been earned, the continuing normal operating expenses, contractual penalties that must be paid due to the delay caused by the covered loss and any necessary additional expenses. However, it’s important to note that this type of coverage does not include the payment of any incentive bonuses that would have been received if the project were completed ahead of schedule.

It’s also possible to add business income, contractual penalties and extra expense coverage. That’s for when a piece of covered equipment is lost or damaged due to a covered cause of loss and the result is that a job cannot be completed. Of course that means a loss of income or a contractual penalty. This coverage will pay the net income that would have been earned, the continuing normal operating expenses, contractual penalties that must be paid due to the delay caused by the covered loss and any necessary additional expenses. However, it’s important to note that this type of coverage does not include the payment of any incentive bonuses that would have been received if the project were completed ahead of schedule.

If you have an arsenal of equipment attachments, it’s important to cover those as well. They can be covered under miscellaneous tools and equipment, but make sure that your limit will sufficiently cover the type of work you do with those attachments. Many attachments can be used by different machines for different applications. So work with an agent to properly define those applications.

With all the daily nuances of machine operation on the jobsite, it’s a good idea to shop around and talk to agents to get your perfect policy. Find out if your formal operator training and certification or preventative maintenance program is reflected in the policy pricing. Does the policy have a deductible wavier when certain theft prevention devices or precautions are in place?

As for how much you’ll typically pay for insurance — that’s a number that’s not easily pinned down. Construction equipment premiums are typically charged based on its exposure to loss. “For example, a crane used on dry land will have a lower premium than one mounted on a barge. The possibility for upset and overturn is greatly increased with water borne exposure,” says Bitler.

Another major difference in your premium would be the expectations you have in a loss scenario. Let’s say that you’re carrying equipment on the books at a depreciation value and the standard insurance valuation is a cash value. If you’re looking for a replacement cost of a new machine, you’re equipment on the books is a lower value, so that would affect your premium. Also, how the machine is outfitted is also a cost factor. Did you spring for the tricked-out cab with air conditioning and satellite radio? That will also affect what you’d pay for coverage.

“Sometimes contractors don’t recognize the difference between coverage for equipment at depreciated value and coverage for the actual cash value of the equipment,” says Tracy. “To alleviate additional burdens that can come at a time of loss, it is imperative that contractors be specific with their list of equipment and make sure that they retain the identification information so that the item is clearly on the schedule.”

The claims process is not exactly fun. Typically, theft claims are seen most frequently, followed by collision and mishandling of equipment by the operator, according to Honeck.

If you do have to make a claim because of equipment loss, it’s good to be armed with excellent records — make, model, serial number, manufacturer identification number and, in the case of a theft, any specific markings that could help identify your machine. Alert your insurance agent as soon as you know about the event.

If you do have to make a claim because of equipment loss, it’s good to be armed with excellent records — make, model, serial number, manufacturer identification number and, in the case of a theft, any specific markings that could help identify your machine. Alert your insurance agent as soon as you know about the event.

“To help expedite the claims process, contractors should keep very good records of the expenses incurred after the loss event. They’ll be assigned a claims adjustor that will analyze the invoices and an expert may even be sent out to see what repairs are necessary,” explains Tracy. “The insurance carrier reviews the repairs and works through the settlement. The speed with which a claim is processed hinges greatly on the communication between contractors and the carrier, the complexity of the loss and the distance from the carrier to the insured, in the case of inspections or jobsite visits. Anything contractors can do to facilitate communication and transfer requested information will expedite the claim.”

Just because you find a policy that fits like a glove doesn’t meant that you’re set for life. Many times contractors will start out the year with certain equipment defined in their policies, but then acquire new equipment and get rid of others. Don’t assume that new equipment is covered. There are specific limits and time frames for reporting new equipment for coverage. So review your fleet with an insurance agent. After it’s all said and done, you’ll have peace of mind that your equipment investment is well protected.

Jason Morgan is Associate Editor of Utility Contractor.

The Benefits of Volunteering

Aflac Explains Voluntary Insurance

Voluntary insurance plays an important role in helping to control employee benefit costs. These policies come at no direct cost to the business and can be a much-needed value-added benefit for construction employers who want to enhance their benefit offerings without breaking the bank. For example, Aflac pays cash benefits to the policyholder, unless they choose otherwise, to help cover daily living expenses due to an accident or illness. The benefits are predetermined and are paid regardless of any other types of insurance policies purchased by the policyholder.

Some of the most common selections include: accident insurance; short-term disability; hospital confinement indemnity; and the cancer plans. These policies provide additional coverage to the policy holder to help manage unexpected expenses due to injury or illness.

In addition to helping construction employers create a more robust benefits package, voluntary insurance products may also provide them with potential tax savings. Aflac’s tax-advantage plans allow employees to use pre-tax dollars to pay for their policies. When businesses can lower the taxable income of their participating employees, they may also reduce their overall share of FICA and FUTA taxes.

Comments are closed here.