America’s IT Construction Challange

The utility industry has been in the news a great deal lately, with much of the emphasis on the energy segment. Concerns about volatile energy prices, environmental regulation and renewable energy have led to a great deal of focus from both government and industry leaders on America’s energy future. America’s communication infrastructure is frequently an afterthought, however, this is changing. Communication infrastructure spending is accelerating, and in the short-term, it exhibits the fastest construction spending growth rate of all the utility segments.

In many ways, the United States’ focus on energy concerns is myopic when evaluating the overall threats to American competitiveness. With the rapid rise of new exploration and production, the United States is now the world’s largest producer of natural gas and the third largest oil producer. New extraction technologies ensure a steady supply of energy with optimistic analysts projecting that domestic production will rise to at point where the United States, Canada and Mexico can be entirely energy independent over the next decade. The United States has a significant natural resource advantage over most countries in the world, but its communications advantages are not nearly as strong.

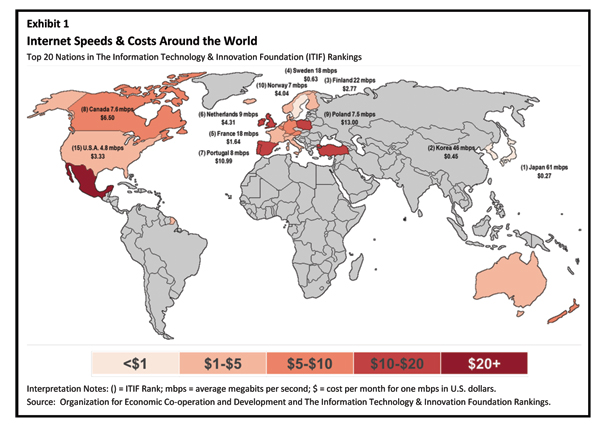

The vast size of the United States provides clear benefits for energy production but can have a negative effect on communication infrastructure. Providing ultra high-speed Internet access across the country is a costly and difficult endeavor. The United States ranks 15th in average connection speed1, lagging behind many European and Asian countries (Exhibit 1).

As more U.S. industries require very high-speed data connections to remain competitive, the relative weakness in this area is a significant threat to our competitiveness. Pressure on U.S. capacity is also increasing. Smartphone usage passed 100 million devices in January 2012 and continues its exponential growth.2 Relatively new products, services and industry changes such as tablet computers, video streaming and datacenter connections will be the next wave of bandwidth consumers.

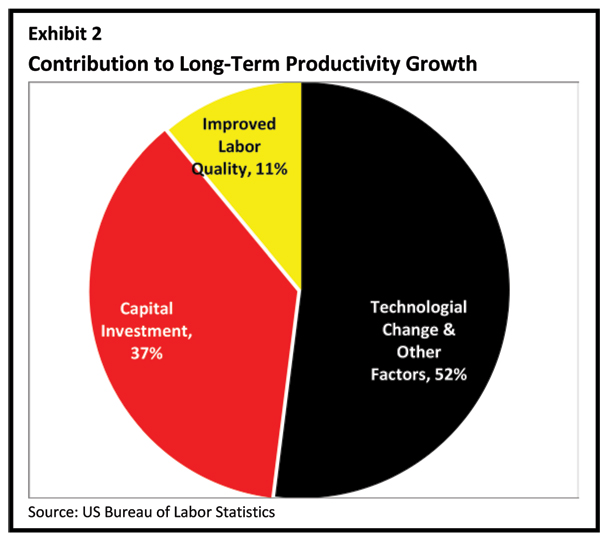

High-speed Internet is a critical factor in U.S. competitiveness. As shown in Exhibit 2, the U.S. Department of Labor indicates that technological change is the largest driver of long-term productivity growth. Productivity growth is itself a driver of wealth creation and competitiveness. In a global and interconnected world, the highest functioning communication system is a critical necessity to maintaining and growing U.S. economic competitiveness.

Unlike some European and Asian countries, it is harder for the United States to approach the need for more communication capacity with a required government-sponsored approach. In February 2011, President Obama rolled out an ambitious blueprint to use $18 billion in federal funds to get 98 percent of the nation connected to the Internet on smartphones and tablet computers in five years.3 The described plan is complicated by requiring multi-agency, multi-state and multi-firm collaboration that will be difficult to implement. Since the announcement, minimal progress has been made on this ambitious plan. However, there is progress in other areas.

Construction activity for this sector has accelerated during 2011 and 2012 due to the spending of nearly $7 billion in broadband related funds set aside in the American Recovery and Reinvestment Act of 2009 (ARRA). Another example is the formation of Gig.U4 in 2011 by 37 leading research universities. Gig.U’s goal is to “accelerate the deployment of world-leading, next generation networks in the United States.” The initiative will use the member universities as test beds for the acceleration and deployment of ultra-high-speed network services and applications. Like most advances in the communications sector, this initiative will begin locally and spread organically in an uneven and often unpredictable way.

Communications Spending Forecast

Historically, communication is the most volatile of all utility industry segments. Along with the rapid growth of mobile device use, data centers and cloud computing are going to be significant industry drivers. Government sponsored rural broadband projects are finally being executed and account for some of the spending growth exhibited in 2011 forward. Overall, $7 billion in government funding has been allocated to this effort.

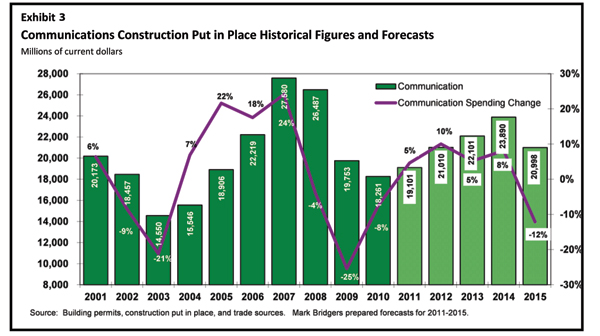

Spending growth from 2004 to 2008 was fueled by wireless demand and the need for more bandwidth to support smartphones (Exhibit 3). The drop in 2009 was primarily related to the poor economy. The forecasted spending increase from 2011 to 2014 is going to be driven by the proliferation of devices requiring both high-speed cellular networks and Wi-Fi access at home and away. This demand is already showing up in the following ways5:

- Corning Inc. sold record volumes of fiber in 2011 and can’t guarantee new orders will be filled.

- Norfolk Southern Corp. is seeing interest in the empty plastic pipes it buried along its tracks in the late 1990s.

- Netflix represented nearly one-third of all peak downstream Internet traffic, up more than 10 percent since last spring, according to network-management company Sandvine Corp.

- Cisco expects the volume of video content crossing the Internet to increase fivefold by 2015 from 2010 levels.

- Pointed in an opposite direction are a number of industry participants warning of a 2000-type overbuild6:

- Andrew M. Odlyzko, a University of Minnesota math professor who warned a decade ago about slower-than-expected Internet growth, says predictions of skyrocketing mobile traffic seem overly optimistic.

- TeleGeography, a telecom market research firm describes plenty of excess capacity available on the nation’s core fiber-optic networks.

- Will Hughs, the top U.S. executive for Australian telecom giant Telstra Corp., which sells long-haul telecom services to U.S. customers, says “A lot of us look at the current construction boom and question if history may be repeating itself.”

Our forecast anticipates a new peak in 2014 followed again by a trough for this industry segment.

Conclusion

Volatility and change is the norm for this sector. The long-term opportunities will be more complicated, competitive and present new challenges to contractors operating in this sector. There is an ancient proverb that goes, “make hay while the sun shines” and the current increases in communication construction spending offer an opportunity to make some hay before clouds on the horizon arrive.

Mark Bridgers and Nate Scott are consultants with Continuum Advisory Group, which provides management consulting, training and investment banking services to the worldwide utility and infrastructure construction industry. They can be reached at (919) 345-0403 or MBridgers@ContinuumAG.com and followed on twitter @MarkBridgers. For more information on Continuum, please visit www.ContinuumAG.com.